Lessons in Fair Lending

Redlining: A Compliance Officer’s Primer

In today’s regulatory environment, most compliance officers are keenly aware of the fact that redlining is one of three 2017 foci for the CFPB and probably for the prudential regulators as well. The purpose of this article is to highlight the key elements in any redlining analysis and thereby make it easier for compliance officers […]Read More »Fair Lending Regression Analysis: Some Frequently Asked Questions

Fair Lending Regression Analysis: Some Frequently Asked Questions Whether you use regression analysis in your fair lending monitoring program or you are thinking about using it, a few regression related questions are asked regularly. This blog will discuss four of the more popular questions. What data do I need? Depending on whether you are going […]Read More »

Learning from the OCC’s Semi-Annual Risk Perspective Report

Last Friday the OCC released its Semi-Annual Risk Perspective report. A key finding of the report is that increased competition among financial institutions has resulted in increased credit risk due to the weakening of underwriting standards as well as the increased layering of risk in credit products such as indirect auto lending. In this environment, […]Read More »Ally Financial Fair Lending Consent Order

By now most compliance officers have heard about the consent order between Ally Bank, the CFPB and DOJ. In short, Ally agreed to pay a total of $98 million in fines ($18 million) and restitution ($80 million) in a disparate impact settlement of an indirect auto lending case. While several law firms and others have […]Read More »DOJ Settlement with Texas Champion Bank

Yesterday the Department of Justice announced a fair lending settlement with Texas Champion Bank, a $345 million bank in Alice, Texas. The allegations concerned pricing on unsecured consumer loans to Hispanic applicants. The settlement was the result of a 2010 referral by the FDIC. In the settlement Texas Champion agreed to pay $700,000 in restitution […]Read More »Community State Bank – Redlining

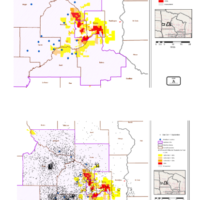

Community State Bank – Redlining Background Community State Bank is a $200 million institution in St. Charles, Mich., (near Saginaw and Flint) with eight branches. Community consented to redlining allegations from the Department of Justice. In the Complaint, DOJ alleged that Community had policies/practices to deny/discourage the residents of majority-minority neighborhoods from obtaining home loans. […]Read More »Ben Bernanke Weighs in on Fair Lending and Housing Discrimination

Ben Bernanke Weighs in on Housing Discrimination Yesterday Federal Reserve Board Chairman Ben Bernanke gave a speech at the Operation HOPE Global Financial Dignity Summit in Atlanta. Bernanke’s remarks were among the most forceful comments about housing discrimination and fair lending that I can remember a Fed chairman making in my more than 20 years […]Read More »Luther Burbank Savings Settlement

Luther Burbank Savings Minimum Loan Amount Settlement On September 12th the Department of Justice announced a settlement with Luther Burbank Savings regarding the setting of minimum loan amounts for home mortgages. Facts · The case originated as an OTS referral to DOJ. · DOJ alleged that through mid-2011 Luther had a minimum loan amount policy […]Read More »

GFI Mortgage Settlement: Not Your Usual DOJ Case

On August 28th the Department of Justice announced the GFI Mortgage settlement that resulted in a restitution fund, a civil money penalty (CMP) and significant administrative requirements. Facts · The case originated as a HUD referral to DOJ, not a referral from a regulator such as the OCC, FDIC, Federal Reserve or CFPB. · DOJ […]Read More »The Cost of DOJ Fair Lending Settlements

There have been several Department of Justice fair lending settlements recently: Countrywide, SunTrust and Wells Fargo specifically. There are likely numerous takeaways from these settlements but let us focus on one of them: cost. To be sure, charges of non-compliance with fair lending rules and regulation can be very expensive. The Cases Calculating the cost […]Read More »DOJ Files Complaint Against GFI Mortgage Bankers

April 11, 2012 Last week the Department of Justice filed a complaint against GFI Mortgage Bankers, Inc. of New York. DOJ alleged “that GFI engage in a pattern or practice of discrimination on the basis of race and national origin by charging African-Americans and Hispanic borrowers higher interest rates and fees on home mortgage loans […]Read More »